Understanding Rent-to-Own & Owner Financing: Risks & Safer Alternatives

For many families, the dream of homeownership feels close—but just out of reach. When traditional mortgages seem unattainable due to credit challenges, lack of savings, or difficulty qualifying, alternatives such as rent to own or an owner finance option can sound like appealing shortcuts.

But while these deals can appear promising on the surface, they often carry serious risks. Without careful consideration, buyers can lose money, face eviction, or even end up worse off than before. As a top Texoma realtor team, Brian & Jonelle of B&J Co. believe in equipping buyers with the knowledge they need to make informed, confident decisions.

What Is Rent-to-Own?

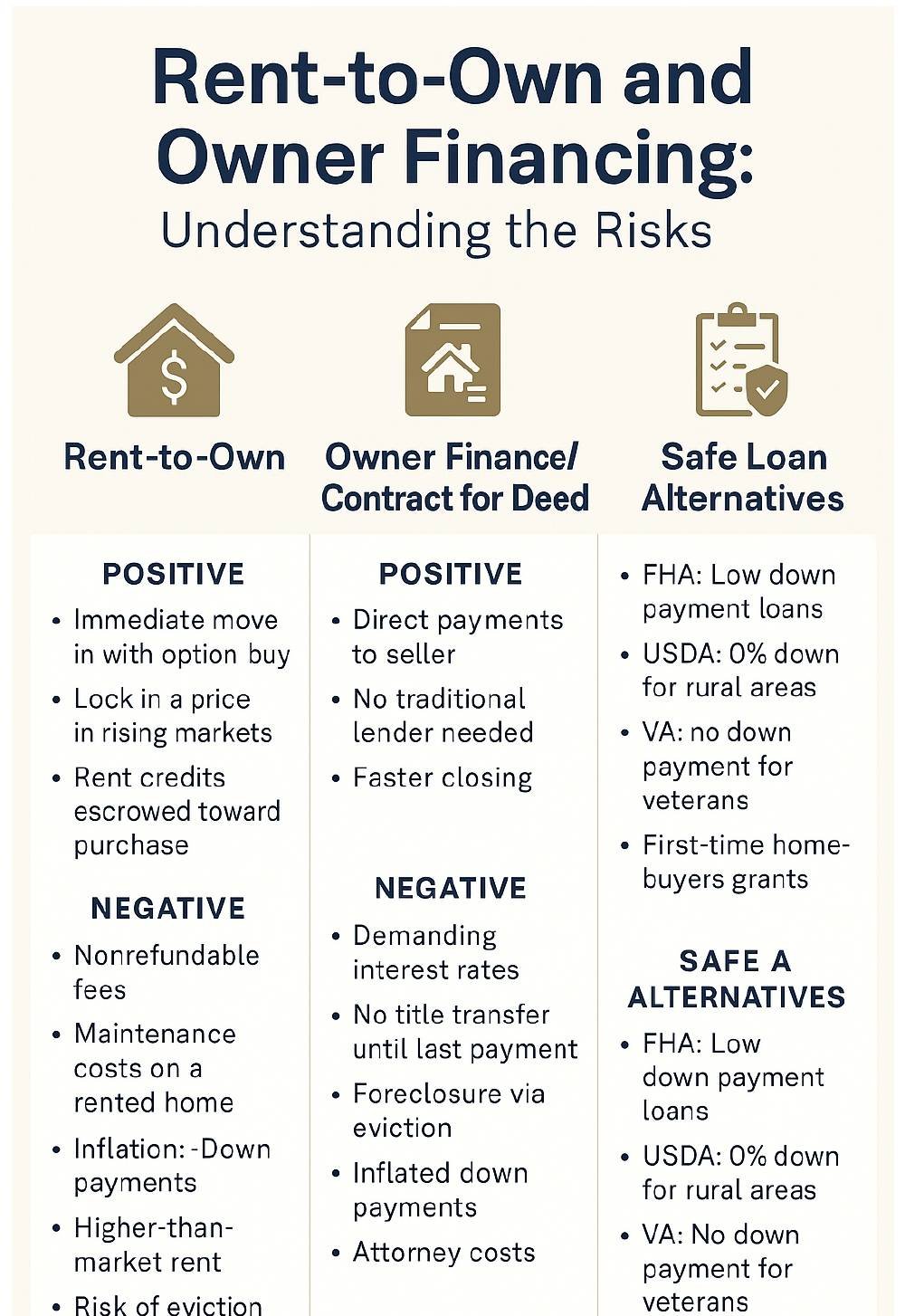

A rent to own agreement is typically a lease combined with an option to purchase. Tenants agree to pay rent for a set period—usually two to five years—with a portion of each payment sometimes credited toward a future purchase price.

The idea of turning rent payments into equity sounds smart. But in reality, many of these contracts place heavy obligations on the tenant. Buyers often take on responsibilities for maintenance, taxes, or insurance even though they don’t hold title to the property. Worse, the contracts are rarely standardized or regulated, leaving renters with little protection if disputes arise.

Understanding Owner Financing and Contract for Deed

Another alternative often marketed as a path to ownership is the owner finance option, commonly structured as a Contract for Deed. In this setup, the buyer makes monthly payments directly to the seller rather than a bank, while the seller keeps legal title until the loan is fully paid.

Key Risks of Contract for Deed

- No Title Transfer Until Final Payment: Ownership doesn’t pass to the buyer until the very last installment is paid.

- Default Consequences: Missing payments can result in the property reverting back to the seller. Unlike traditional mortgages, foreclosure protections may not apply.

- Eviction vs. Foreclosure: Buyers often face eviction instead of foreclosure, meaning far fewer legal safeguards.

- Timeline Pressure: If financing cannot be secured or the balance isn’t paid after the agreed period, the deal ends and the buyer loses their investment.

- Legal Costs: Enforcing or disputing a Contract for Deed often requires attorneys and court appearances, driving up costs.

- Higher Interest Rates: Owner financing deals frequently come with above-market interest rates, making long-term ownership more expensive.

- Credit Limitations: On-time payments don’t usually get reported to credit bureaus, so the buyer’s credit score may not improve despite years of consistent payments.

- Inflated Down Payments: Many contracts demand large upfront option fees or down payments well above what buyers can afford.

Common Pitfalls in Rent-to-Own

- Unregulated Contracts – Agreements often lean in the seller’s favor.

- Hidden Property Issues – Without appraisals or inspections, buyers can overpay for homes with major defects.

- Maintenance Burden – Tenants frequently shoulder the cost of repairs while still technically renters.

- Uncertain Property Status – If the seller has unpaid taxes, liens, or even their own mortgage default, the renter’s rights may be wiped out.

- Forfeited Money – Any option fee or rent credits are often nonrefundable if the tenant cannot complete the purchase.

- Inflated Down Payments – Buyers are often asked for upfront money well beyond what they’d need for a safer FHA or USDA loan.

If You're Still Considering Rent-to-Own

Important: If you're determined to pursue this path, protect yourself by working with a trusted attorney and a top Texoma realtor who can advocate for fair terms.

Potential Positives

- Immediate occupancy while working toward ownership

- Flexibility to lock in today’s price in rising markets

- Opportunity to improve credit while renting

- A sense of stability compared to traditional renting

Significant Negatives

- Option fee and rent credits are often nonrefundable

- Monthly payments are usually higher than market rent

- Buyers carry repair costs despite not owning the home

- Risk of eviction if payments are missed

- Inflation-adjusted down payments and higher interest rates

- Payments typically do not build credit history

Safer Alternatives for Buyers

For buyers exploring homes but unsure how to finance, there are safer paths than rent-to-own or owner financing:

- FHA Loans – Low down payment (3.5%) with credit scores as low as 580.

- USDA Loans – Zero-down payment mortgages for eligible rural areas.

- VA Loans – Zero down with no PMI for veterans and active-duty military.

- First-Time Buyer Grants – Many state and local programs provide closing cost assistance and down payment aid that doesn’t need to be repaid.

Final Thoughts

While rent to own and owner finance options may sound like a quick fix, the risks—eviction, forfeited money, inflated down payments, attorney costs, higher interest, and no credit reporting—make them dangerous for most buyers.

If you’re still considering these paths, do so only with full transparency, legal protections, and a trusted guide by your side. Better yet, consider FHA, USDA, VA, or 1st time home buyers grants for true help with buying a home.

With Brian & Jonelle of B&J Co., your top Texoma realtor duo, you can explore homes with confidence and secure a safe, sustainable path to ownership.